The global aviation industry incurred losses of $371 billion in gross passenger operating revenues in 2020, compared with 2019, as airplanes across the world were grounded during the Covid-19 induced lockdown. The International Civil Aviation Organization expects airlines to post $296-317 billion in losses during 2021. Yet, across the world investors are on the hunt to fund start-up airlines.

“Over 90 start-ups are planning to launch new airlines and there is a lot of risk equity capital chasing these start-ups,” says Kapil Kaul, CEO and director of CAPA Advisory, a global aviation consultancy firm. India, he believes, may well see a few start-up airlines in the near term. Already leading stock market investor Rakesh Jhunjhunwala is gung-ho about promoting a new airline — Akasa — and talks are on for the possible revival of grounded carrier Jet Airways by U.K.’s Kalrock Capital and U.A.E.-based entrepreneur Murari Lal Jalan. The Tata Group is also considered to be frontrunners in the disinvestment of debt-ridden Air India.

So, what is the attraction in launching airlines at such a time? The advantage that start-up airlines have, according to Kaul, is cleaner balance sheets and a very competitive cost base — costs related to aircraft ownership are cheap and manpower is affordable. “This opportunity is uniquely created by this crisis,” says Kaul.

With an estimated net worth of over $4 billion, Jhunjhunwala has gone on record to state his intentions of venturing into India’s bloodied aviation market. Domestic airlines are expected to post a consolidated loss of $4.1 billion in FY22, similar to what they incurred in FY21.

“One-third of my wealth is in unlisted equities,” Jhunjhunwala had said, while speaking at a virtual panel discussion organised by investment bank Equirus in July. “I also invested in 14-15 companies and am now promoting a new airline,” added Jhunjhunwala, who runs private equity and asset management firm Rare Enterprises. A detailed e-mail sent by Fortune India to Jhunjhunwala on his imminent entry into the aviation market did not elicit a response.

What is publicly known is that Jhunjhunwala plans to promote ultra low-cost carrier (ULCC) Akasa with an initial investment of $35 million. Former IndiGo president Aditya Ghosh and former Jet Airways CEO Vinay Dube would be part of this venture, which has applied for an air operators permit. The initial fleet size is around 70 aircraft.

In absolute terms, Jhunjhunwala’s planned investment in Akasa is sizable, but relative to his networth it’s “not even a rounding error,” says Satyendra Pandey, managing partner at aviation advisory firm AT-TV. But Jhunjhunwala’s entry does provide the opportunity for a new airline to be well-capitalised, attract good talent, and start with scale. Something that new promoters of Jet Airways may struggle with.

In fact, a former Indian aviation executive is quite sceptical about Jet Airways’ second take-off even after getting a go-ahead from the National Company Law Tribunal. “The name may be re-used, like Pan Am was used multiple times by fringe start-ups, but it makes zero sense to revive an airline with huge liabilities, very few assets, and in a crowded market in a pandemic,” he says on condition of anonymity. He also questions the viability of the ULCC model that Jhunjhunwala is toying with. Where would the lower costs come from in the context of the Indian market? “IndiGo has one of the lowest cost structures in the world. Don't see how a new airline can be any more low-cost than an IndiGo with its scale and purchasing power,” the former aviation executive adds.

Kaul points out that a ULCC model needs to focus on lower distribution costs by way of direct sales channels, higher aircraft and pilot utilisation, strategic negotiations with aircraft makers for lower maintenance costs, a reduced employee bill by linking part of compensation to performance, and digitisation across operations.

Now if you look at the cost structure of an airline in India, there is very little that any new start-up can do on fuel. Despite IndiGo having the lowest cost per available seat kilometre in the industry, fuel costs—having doubled over last year—impacted the airline’s April-June quarter financial performance by ₹540 crore. It reported a loss of ₹3,174 crore during the quarter. At airports, too, there isn’t much room for manoeuvrability for a start-up, as secondary airports close to major metros are almost non-existent.

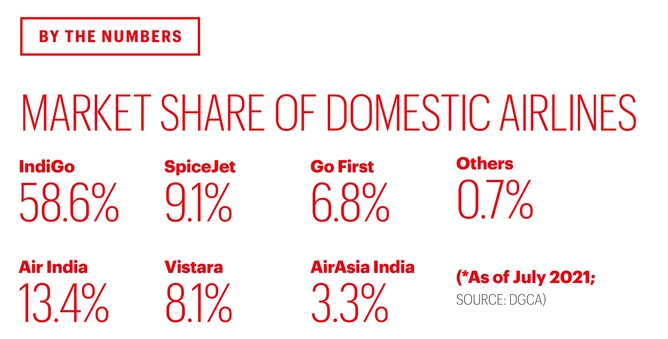

When it comes to ticket distribution the key channel remains OTAs (online travel agencies) such as makemytrip. “And they are very powerful,” says Pandey of AT-TV. “Even IndiGo with 58.6% market share has not been able to displace them. It remains to be seen how a ULCC player would disrupt that.”

The model also operates on lower ticket revenues, which means ancillary revenues are key. At present, the Directorate General of Civil Aviation does not allow any extreme unbundling of fares that ULCCs depend on, like charging for water.

Industry watchers expected that one or two airlines in India would shut shop a year into the pandemic. However, that has not happened, even though some are operating at half their capacity or even less. This makes it harder for a new airline to get a head-start or advantages. But that may change once the pandemic fears recede and travel opens up.

“It will be a test of endurance for the founders,” says Kaul.

Leave a Comment

Your email address will not be published. Required field are marked*