In June 2020, Praveen Khandelwal, secretary general of Confederation of All India Traders (CAIT), the apex body of Indian traders, said its 80-million members will not buy or sell goods from China. This was the result of growing anti-China sentiment in sections of pro-BJP organisations, including the ruling party’s ideological mentor Rashtriya Swayamsevak Sangh and its affiliates Swadeshi Jagran Manch (SJM) and Vishwa Hindu Parishad. One reason was skirmishes between Indian and Chinese armies in border areas. Another was Covid-19, which had originated in Wuhan in China and caused global supply chain disruptions. There was also the huge trade deficit and dependence on raw material from China for making several essential goods, including life-saving medicines. All this made government, too, realise the need to find alternatives to Chinese imports.

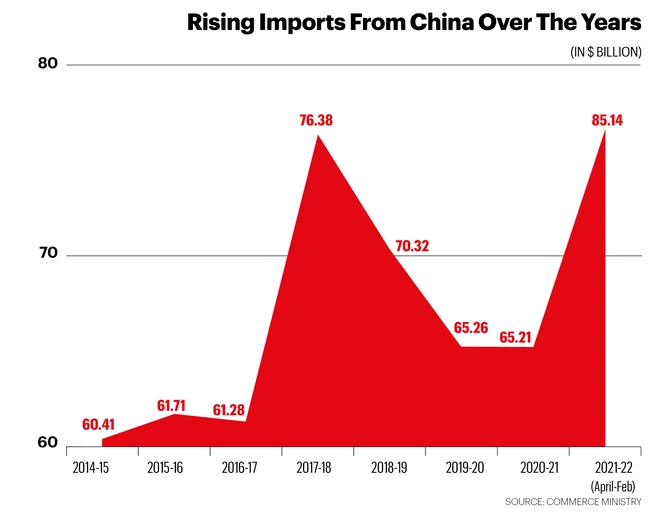

However, value of goods imported from China touched an all-time high of $85.14 billion during April 2021-February 2022. The last time Chinese imports had touched this level was in FY2018 ($76.38 billion). Imports from Hong Kong make these numbers even bigger. During April 2021-February 2022, India imported $17.24 billion worth of goods from Hong Kong, higher than $13.57 billion in April 2021-February 2022 period. Combined imports from China and Hong Kong touched $102.38 billion in the first 11 months of FY2022.

Coming after loud anti-China campaigns by traders and civil society groups, government’s initiatives to reduce trade imbalance, Centre’s high-profile pitch for atmanirbharta (self-reliance) and ambitious production-linked incentive (PLI) scheme to promote local manufacturing, these record imports pose a big question: Did government’s attempts and citizens’ resolve to reduce Chinese imports fail?

There are no straight answers. The surge in import numbers is more complex than it seems. First, increase in value of total imports does not always reflect product-specific volume trends. There are sectors where imports from China—both in value and volume—have declined. There is also a subtle but positive change in the type of products being imported—less finished goods and more raw materials and intermediate goods. The boycott has had an impact, but irrespective of whether Indian consumers boycott Chinese goods or not, China remains, and will remain in the foreseeable future, the main source of raw materials for Indian industry.

The Surge

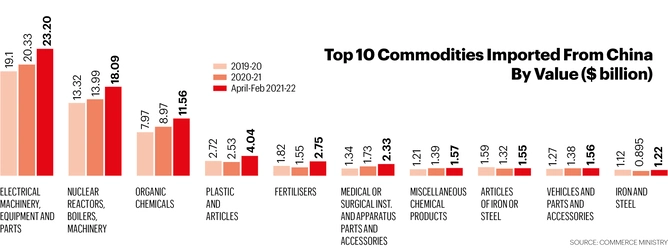

A glance at commerce ministry data shows that every item in the list of top 10 merchandise imports from China has gone up in value. India imported electrical machinery and equipment worth $26.01 billion in the first 11 months of FY2022, higher than $20.33 billion during FY2021. The category of nuclear reactors, boilers and machinery (largely the latter) saw imports worth $18.09 billion during the April-February period, higher than $13.99 billion for the entire FY2021. Imports of organic chemicals, the third most valuable item in the list, were $11.56 billion, higher than $8.97 billion in FY20. “There are various explanations. One, there is suddenly a spurt in economic, manufacturing activity (post Covid-19 disruption) because of which demand for raw materials and intermediates has picked up. Second, in last one year, government has acted against under-invoicing. With (tax) evasion under attack, the value has gone up. Thirdly, there is increase in prices, especially of electronic products,” says Ashwani Mahajan, national co-convener, Swadeshi Jagran Manch (SJM), adding, “You can’t make sweeping remarks (on reasons for the import surge).”

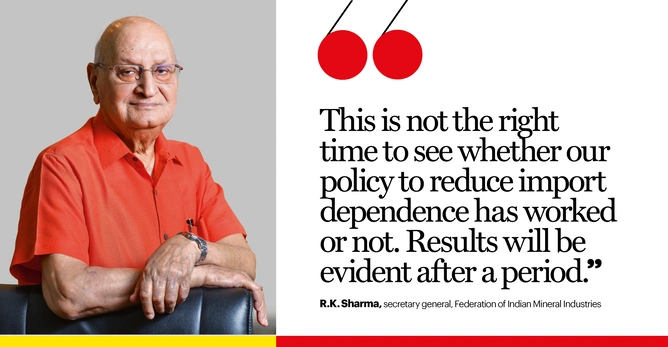

R.K. Sharma, secretary general, Federation of Indian Mineral Industries (FIMI), says while there has been an increase in mineral and metal imports from China, one cannot qualify it as good or bad. “Increase in overall consumption in our country is the major reason for this. Our (mineral) production is not meeting our demand. This is not the right time to see whether our policy to reduce import dependence has worked or not. Government schemes are in place, results will be evident after a period. How long? We can’t say now, but two or three years are certainly not enough. May be, for some products, five years are enough, for others, 10 years, and for others, even more,” says Sharma.

In fact, metals and minerals, including coal, accounted for about 25.4% imports from China. Value of mineral imports, excluding coal, is four times the value of domestic production. As per data from mines ministry, in 2016, only 114 out of 154 mineral blocks offered could be auctioned. Out of those, even after six years, the 63 greenfield projects are far from operational. FIMI points out that India is 100% dependent on imports for several metals such as nickel, cobalt, lithium, germanium, strontium, rhenium and beryllium. China remains a key source for these metals.

One more reason for increase in prices of some products is anti-dumping duty. India has initiated at least 30 anti-dumping investigations in last two years against products from China. Industry points at least one instance where lifting of anti-dumping duty increased imports from China. “We had an anti-dumping duty on basic raw material to make MMF (man-made filament) fibre. Two or three years ago, government removed that. Polyester in India is expensive in comparison to China because basic raw material is expensive (in India). Since the world is switching over to MMF, people were importing (the raw material) from China,” says Rajesh Masand, president, Clothing Manufacturers Association of India. He says FY2021 was also the period of dip in India’s MMF production. Government has, in fact, announced a PLI scheme to promote local production of MMF, though it will take a couple of years to make a difference.

Another big product category where import growth is evident is basic chemicals. Nipun Jain, promoter of New Delhi-based pharmaceutical firm Pharmchem, says he is not sure if there has been an increase in import volumes, but prices of imported key starting materials and intermediates have more than doubled in last three years. “Erythromycin thiocyanate, which was $55-60 a kilo, has gone up to $85. N-methylpiperazine was at $5.4 a kilo just one year back. Today, it is at $15.4,” says Jain. Prices of even a common product like citric acid, used by the food and pharmaceutical industry, have shot up from ₹60 a kilo to ₹210 a kilo.

Positive Signals

High raw material prices are an issue, but non-availability is a bigger problem when these imports are used to make finished goods, as in pharmaceuticals. Ajay Sahai, director general and CEO, Federation of Indian Export Organisation (FIEO), says some imports from China are vital for India’s economy. “The basic strategy should be to look into finished products that China is supplying and see whether we can substitute them with products made domestically. If you are importing fertiliser or coal to meet the economy’s requirements, I don’t see any problem. It should be finished goods that we must be careful about,” says Sahai.

A preliminary analysis of China’s imports and exports by Murali Kallummal, professor (Tariffs, Standards, and FTA), Centre for WTO Studies, Indian Institute of Foreign Trade, suggests there is good news hidden behind broad numbers showing rise in imports. When we disaggregate data into intermediate goods, raw materials, capital goods and consumer goods, we find that volume and price rise has been more pronounced in raw materials than other categories. Import of more raw materials—as opposed to finished products—indicates greater value addition within the country. At $27.46 billion, import of finished capital goods during FY2022 (April-November) is yet to cross the $29.69 billion figure touched in FY2021 or $28.07 billion in FY2020. However, India imported raw materials worth $812.1 million during April-November FY2022, much higher than $497 million in FY2021 and $637.4 million in FY2020.

Similarly, India imported consumer goods worth $10.17 billion in FY2022 (April-November), lower than $13.61 billion in FY2021 and $14.55 billion in FY2020. Intermediate goods follow the same pattern. At sectoral level, Kallummal’s analysis shows that in case of electrical machinery, finished goods (or consumer goods category) imports during April-November FY2022 were $4.94 billion, lower than $7.14 billion in FY2021 and $6.52 billion in FY2020. There is similar trend in consumer goods category, non-electrical machinery, minerals and metals and chemicals.

Kallummal also tracked changes in unit prices. Though unit price is merely indicative as the unit is different (kilo, litre, etc) for different products, it can show if increase in value of imports is only due to price increase or imports have risen in volume too. A rise in unit value indicates that import cost has gone up irrespective of import volumes. However, one reason for increase in unit value could be minimum import price-based measures imposed by the government.

The analysis shows that the unit value of capital goods in general came down from $17.2 in FY2021 to $15.9 in April-November FY2022. The value fell in electrical and non-electrical machinery but rose in minerals and metals. The change was more prominent in consumer goods. While the overall unit price declined from $5.7 to $4.2, the change was very clear in case of chemicals (consumer goods category)—from $3.2 in FY2021 to $2.7 in April-November 2021. Kallummal’s analysis also shows rise in unit prices of raw materials. Overall, the price went up to $2.8 in FY2022 (April-November), from $1.7 in FY2021 and $1.9 in FY2020. The steepest increase is in minerals and metals that come under the raw material category, $4.6 in FY2022 (April-November), from $2.2 in FY2021 and $2.5 in FY2020. Kallummal carried out a similar exercise to understand import trends from Hong Kong. The average unit price followed the same pattern as imports from China in capital goods, consumer goods and intermediate goods. The only category where there has been an increase in unit price in April-November FY2022 is raw materials. But one should keep in mind that the period of increase is not a complete year and may change.

A recent online survey by community social media platform LocalCircles illustrates this further. A total of 39% households said they have not bought made-in-China products in last 12 months. Out of households which bought China-made products during the period, 67% said they have reduced their purchases as compared to a year before. The survey also found out that “gadgets and electronic/mobile accessories” are the top categories where Indians buy Made-in-China products. The survey indicates the impact of boycott calls over the last couple of years. Hard numbers also suggest reduction in import of popular consumer goods like toys or consumer electronics from China, though the reduction gets nullified by increase in import of raw materials and intermediate goods.

Imports from China are at a record high, but that is not necessarily all bad news.

Leave a Comment

Your email address will not be published. Required field are marked*