MUMBAI’S LEGENDARY Sea Rock Hotel embodies both the missteps of The Indian Hotels and its probable path to redemption. Spread over more than six acres of land abutting the sea in Bandra, Sea Rock was where Bollywood hung out in the late ’70s, ’80s, and early ’90s. Ramma Bans ran Sea Rock’s gym where Rekha came for her workouts. (They even produced a fitness video together). Subhash Ghai hosted his after-release parties there, while the Amitabh Bachchan starrer Don wasshot in its banquet hall, complete with a red velvet background and large chandeliers. Built by the four Luthria brothers in the ’70s, managed by the ITC-Welcomgroup, and later franchised to Sheraton, Sea Rock was one of the few five-stars in Mumbai.

In 1993, terrorists blew up parts of the hotel, which was then shut down. In 2005, the Luthrias sold it to the Nandas, who run the Claridges hotels in Delhi and Faridabad, for an undisclosed sum, reckoned to be between Rs 180 crore and Rs 300 crore. The Nandas tried running Sea Rock with a limited number of rooms, but gave up after a year and a half. The U.S.-based Mandarin Oriental Hotel Group was then interested in the property, but eventually the Nandas sold it to Indian Hotels for Rs 700 crore in 2009.

Sea Rock sits across the road from Indian Hotels’ other property in Bandra, Taj Lands End. Till the turn of the millennium, most of Mumbai’s commerce was concentrated in the south. But high real estate prices, combined with the lack of space, forced many companies to relocate to areas in, around, and beyond Bandra. What was once the suburbs is now ‘north Mumbai’. So buying Sea Rock seemed like a smart move—till Umesh Luthria, one of Sea Rock’s former owners reveals that he and his family took the deal to Indian Hotels before they took it to the Nandas. “But they were seemingly uninterested.” One reason could have been the undeveloped space within the precincts of Lands End. While he doesn’t disclose the price he offered, it’s safe to assume that it would have come a few hundred crores cheaper than what Indian Hotels ultimately paid.

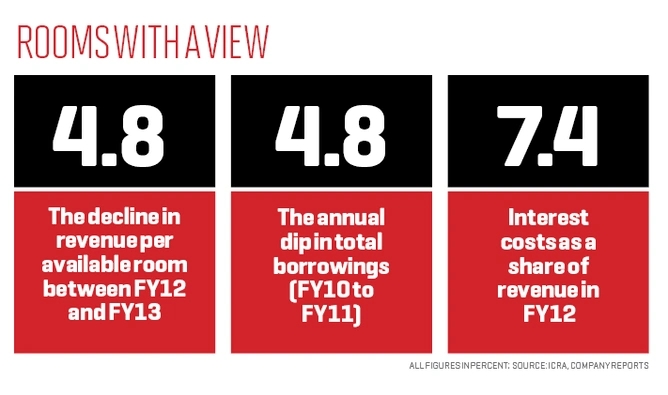

Former employees say the company lacked the foresight to build rooms in north Mumbai even as recently as the mid-2000s. “It focussed on its three south Mumbai properties,” says one. In the last five years, the revenue per available room (revPAR), the most significant hotel industry statistic, has halved to Rs 4,950 among five-star hotels in south Mumbai, according to HVS, a hospitality industry research outfit. More significant, newer properties of hotels such as the Hilton, JW Marriott, and Grand Hyatt, have added more than 2,500 five-star rooms in north Mumbai in the past decade. Indian Hotels’ sole offering in the north continues to be the 493-room Lands End.

Rebuilding Sea Rock is now high on the agenda as it will re-establish Indian Hotels as a serious player in north Mumbai. The hotel was demolished in 2010, and the group applied for building permission. “Of the 20 odd CRZ [coastal regulatory zoning] licences, we’re lacking approval for one,” says Anil P. Goel, Indian Hotels finance director. One plan is to connect Sea Rock to Lands End. Together, the two will account for 1.5 million sq. ft. of space, with the new hotel adding 1,000 keys, luxury residences, serviced apartments, 12 restaurants, two large ballrooms that will hold 2,000 people each, and two smaller ones for 800 and 400 people.

The trouble is that all costs combined—acquisition, opportunity cost, cost of building, etc—may make the project unviable for years. “You have to watch your costs on the land you are buying because an expensive hotel on cheap land makes sense, but an expensive building on expensive land isn’t the best way to go,” says Adarsh Jatia, managing director of Magus, the company which owns the Four Seasons property in Mumbai.

Goel agrees that the delay is costing them “because the holding cost is not small change”. Sea Rock is currently held outside the Indian Hotels balance sheet via a special-purpose vehicle. In its last report in November 2012, credit rating agency ICRA referred to the substantial funds that will be required to rebuild Sea Rock and that its funding would influence ratings in the medium term. The same report notified ICRA downgrading one of Indian Hotels’ debt instruments from AA+ to A+.

The last decade hasn’t been kind to India’s oldest and largest hotel company. Sure, it made plenty of headline-grabbing deals such as buying The Pierre in New York and the Ritz Carlton in Boston, but these haven’t added much to the bottom line. Instead, they have weighed it down with debt. Many of the assumptions that went behind Indian Hotels’ bid to become a global player have proved untrue. Worse, the biggest hotels in the world—Hyatt, Marriott, Hilton, Four Seasons, etc.—have all begun creating capacity in India, which still accounts for over 70% of Indian Hotels’ revenue. A Hong Kong-based senior executive from Hyatt, who asked not to be named, says that in the next five years, Hyatt will be building some 60 hotels across Asia, of which more than half will be in India. In January, the Carlson Rezidor Hotel Group, which owns Radisson and is the largest foreign operator in the country with 63 hotels, announced a 100-property target.

The head of one of India’s largest travel agencies, who asked to remain anonymous because Indian Hotels is a client, says the company is trapped between the cookie cutter model of the Hilton, which has more than 100,000 rooms across the world, and luxury players such as Mandarin Oriental.

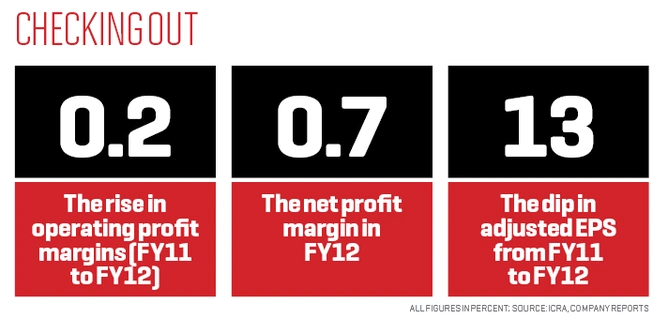

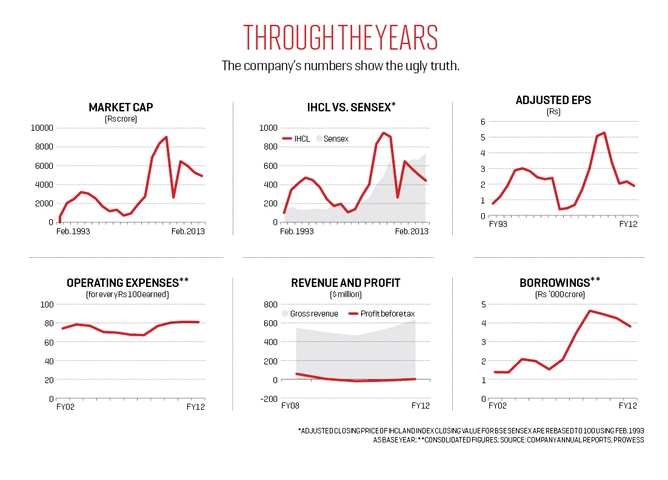

Raymond Bickson, Indian Hotels’ managing director and CEO, says international chains often don’t convert their promises to reality. He claims that one in three projects don’t happen. “Hotel companies can say whatever they want.” That may be true, but the markets don’t have much faith in Indian Hotels either. Its adjusted earnings per share is the lowest in five years, while nearly Rs 5,000 crore of market capitalisation has been wiped out over the same period. The return on capital employed stood at 4.8% in FY12. Among the top 10 Tata group companies, Indian Hotels’ shareholder returns have been one of the poorest at -45%; only Voltas and Tata Communications have fared worse.

Rashesh Shah, analyst with ICICI Direct, who has a negative hold rating (expecting the stock to underperform), says the revPAR and average room rate suggest that “the overall performance is likely to remain tepid”. He adds that if Indian Hotels pursues buying a major stake in Orient-Express Hotels, it will squeeze profitability further. In 2007, Indian Hotels picked up 10% of Orient-Express for $209 million (Rs 1,123 crore at current rates) as a run-up to buying a majority stake in it. Orient-Express has so far rebuffed all overtures, including a bid to buy the company for $1.2 billion in December. Meanwhile, the value of Indian Hotels’ holding in Orient-Express has dropped 85%, but it hasn’t given up hopes of owning more.

Analysts are also worried about the cost needed to renew the lease of its Delhi flagship—The Taj Mahal Hotel, Mansingh Road—due in October, given that other companies are also eyeing it and will up the ante. Indian Hotels doesn’t discuss the issue.

In a presentation made to Fortune India on Indian Hotels, Bickson explained, among other things, why shareholders should stay invested. His pitch was in generalities that revolved around the company’s heritage, the boom-and-bust cycles it has endured, and the assets it owns. Come June, Bickson would have been running the company for 10 years, after which his contract comes up for renewal. The gains in the first half of his stewardship have been mostly destroyed in the second. He doesn’t exactly own up to management missteps but, along with other senior members of his team, admits that there are parts of the business that make him deeply unhappy. Goel, who has the onerous task of defending his company to the financial community, says, referring to the U.S., where the company invested heavily, “We are happy with the assets acquired, but are obviously not very happy with their performance.” He adds that they have a lot to do before the properties give “economic returns”.

Beyond such statements, it’s the company’s moves that point to a rethink. Bickson talks of pushing ahead an asset-light expansion model, while Goel says Ginger Hotels, the group’s budget hotel chain, will be spun off through a primary issue. Many question why Ginger should be a part of Indian Hotels at all.

It’s not clear how Cyrus Mistry, the new chairman of Tata Sons, the group’s holding company, thinks about the role of hotels in the $100 billion Tata group. While his personal wealth is invested in it—his family owns 18% of Tata Sons, which, in turn, owns 20% of Indian Hotels—he has been in the job barely three months. In an e-mail reply, the company said that historically, its promoters have been “extremely supportive” and “we will thus continue to benefit from the strategic vision and guidance from Mr. Mistry”. Hotels had an emotional appeal for his predecessor, Ratan Tata: It is one of two businesses remaining which was started by founder Jamsetji (steel is the other).

To demonstrate faith, in the last few months of Ratan Tata’s tenure, Tata Sons converted some 48 million warrants of Indian Hotels into 0.35% shares at a premium to market. It’s doubtful, therefore, if Indian Hotels will ever bring in a partner to help re-evaluate how it runs the business, unlike competitor East India Hotels (the Oberoi chain) which almost picked Four Seasons as a partner. All fixes will have to come from within.

THE FIRST EVER TAJ HOTEL—the Taj Mahal Palace on Mumbai’s western seafront—opened its doors on Dec. 1, 1903. An advertisement in a daily proclaimed its “luxurious furnishings, all the latest comforts for moderate charges of Rs 6 upward”. A fervent nationalist, Jamsetji wanted to build a world-class hotel which wouldn’t discriminate against Indians. From Mahatma Gandhi, who entered its portals in the summer of 1931 and refused to use the lift to attend a clandestine political dinner organised by Sarojini Naidu for young Europeans sympathetic to India’s call for freedom, to jazz great Duke Ellington, to Beatle George Harrison, to countless heads of state and other heavyweights, the Taj Mahal Palace has hosted them all. While this has generally worked to the advantage of Indian Hotels, the legend has sometimes attracted the wrong sort. Such as the terrorists, who tried blowing it up on Nov. 26, 2008, because it was seen as a shining symbol of India.

The contemporary history of Indian Hotels has been shaped by three men: Ajit Kerkar, R.K. Krishna Kumar, and Bickson. Kerkar ran it between 1970 and 1997 and grew it from a Rs 2.7 crore, one-location hotel, to more than 42 hotels, with operations overseas and a revenue of Rs 1,000 crore. J.R.D Tata, who headed the Tata group through most of Kerkar’s reign, generally left him alone. But after Ratan Tata became chairman in the early ’90s, Kerkar famously clashed with him and was ousted.

Ratan Tata then picked Krishna Kumar to run Indian Hotels. He’d shot into fame a few years earlier when, as the head of Tata Tea, he’d orchestrated India’s first leveraged buyout, snapping up Britain’s Tetley. Unlike Ajit Kerkar, Krishna Kumar was no hotelier. His common refrain was that he was an “obedient soldier of the Tatas”. (He’s been with them since 1963.) He was more of a manager, who began cutting back the excesses committed in the name of hoteliering. Expenses now had to be pre-approved and there was scrutiny on the use of hotel resources. He cut budgets for suits and apparel for senior managers (grade 9A and above) and curbed international telephone calls. A former employee recalls that during the launch of the Taj Exotica in Goa, a manager made a presentation detailing how 150 employees were required, and that 75 had been hired so far. “Hire a single person more and I’ll fire you,” was Krishna Kumar’s response. Sanjay Sethi, a former area director for Taj Hotels, Hyderabad, who worked with Indian Hotels for 14 years says Krishna Kumar “shocked the system, but built good initiatives like the Tata Business Model of Excellence—a formal system that builds quality”.

Some former employees say the efficiency drives came at a cost, given that hotels are a people-driven business. “The motivation and the level of enthusiasm related to service move parallel to how empowered people are made to feel,” says Shashank Warty, senior vice president, corporate affairs at Indian Hotels until 2006. (Despite repeated requests, Krishna Kumar wasn’t made available for interviews.)

Meanwhile, Bickson joined as managing director in 2003, with Krishna Kumar playing vice-chairman. Indian Hotels was looking for a CEO with global experience and the American from Honolulu seemed the right fit. It was a huge break for Bickson: Previously he’d been general manager at the Mark Hotel, a 170-room, single-location, five-star in New York. He was now given charge of a multi-location behemoth with thousands of rooms.

DECONSTRUCTING INDIAN HOTELS’ recent performance raises many questions. Was its strategy flawed? Or was it merely its execution? Or was it both? How much did the economy blindside the management? Did the business complexity overwhelm the executives? The answers are instructive for all aspiring multinationals from emerging economies.

For most of its life, Indian Hotels functioned in an oligopoly in which three chains—Indian Hotels, East India Hotels, and ITC-Welcomgroup—controlled 60% of the market. Of the three, Indian Hotels was the largest, with a 25% share. A former senior executive from East India Hotels, who now runs his own chain, says for all the players, adjusting to heightened competition wasn’t easy. Today, there are 41 brands fighting it out. “We were suddenly competing against hotels, many of which were from the U.S., arguably the toughest market in the world,” he says. Compared to India’s 173,000 hotel rooms, the U.S. has nearly 5 million, servicing a fourth of the population.

In interviews he gave to the media soon after he joined, Bickson read the threat thus: Foreign brands would direct traffic to their own hotels in India, and would segment the Indian market. He also saw a need to de-risk the India story. Looking back, Bickson says he was familiar with how two legendary Japanese players—Okura Hotels and Imperial Hotels—had lost control over their domestic market with the advent of foreigners after half a century of dominance; he didn’t want that happening to Indian Hotels.

The response fitted nicely with the overall Tata strategy. In the early 2000s, the Tatas began contemplating an overseas push. The reasons varied from having access to better technology, to building a global supply chain to de-risking India’s economic cycles. “Krishna Kumar led the charge from the front for the Taj,” recalls Partha Chatterjee, a former employee, who was director of sales for the western region and regularly met Kumar.

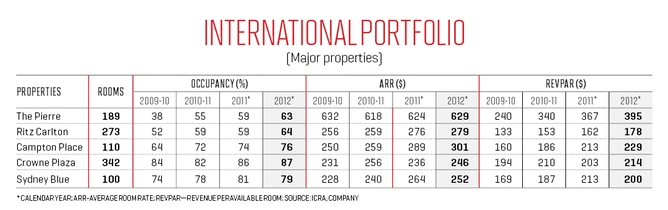

In 2005, Indian Hotels bought The Pierre in New York for Rs 200 crore and the W Sydney for Rs 126 crore; the following year it was the Ritz Carlton in Boston for Rs 765 crore, which was followed by the Campton Place in San Francisco (Rs 270 crore) in 2007. The company saw these, especially the U.S. cities, as gateway destinations from where disproportionate traffic to India arrived. Earlier, the company had unsuccessfully bid for New York’s Carlyle Hotel and Singapore’s Raffles.

The Tatas weren’t just pushing globalisation. They were also investing in bottom-of-the-pyramid innovation. The Nano (car) is the most celebrated example of this. Indian Hotels’ version of the Nano was Ginger, a no-frills hotel chain, launched in 2004.

Significant sums were poured in. According to markets database Prowess, between FY02 and FY12, Indian Hotels’ total capital employed steadily increased from Rs 2,610 crore, peaking at Rs 8,167 crore in 2009, before falling to Rs 7,477 crore in 2012. Goel says, around 2008, Indian Hotels had an Ebidta of around Rs 985 crore, great for a mid-sized company, and they figured they could absorb losses from the new projects without any adverse impact. The markets played along and in the first few days of January 2008, the company’s value reached an all-time high of over Rs 10,000 crore. Krishna Kumar and Bickson appeared vindicated. Over the next five years, Bickson’s remuneration rose 12% annualised to touch Rs 8 crore in FY12. (In an e-mailed statement, the company says while it benchmarks compensation, starting in 2009, there were voluntary cuts in annual bonuses for senior management as well as foregoing annual increases.)

While nothing was wrong with the strategy, a closer look reveals that Indian Hotels was buying assets at the height of the real estate boom in North America. In other words, all that cash was going into a market that sooner or later would go just one way: south. (The other big Tata buys in that period, Jaguar Land Rover and Corus, were at fire sales.) As Goel says, the trouble with hospitality is that there “is a total disconnect between the valuation of real estate and the cash that it generates”.

Others point to hubris. Take The Pierre, one of the properties that continues to drag profits down. When Indian Hotels took it over from Four Seasons, which ran it for 18 years, it committed to invest around $35 million against a 30-year lease. Soon after, it increased its budget by another $70 million, taking the total outlay to three times the original amount. Most hotel developers say anything beyond a 2% or 3% variation means the management wasn’t paying enough attention. Indian Hotels sees it differently. Goel says renovation expenses didn’t just spiral up, but were deliberately raised.

Once an in-principle agreement with the owner was reached on how much Indian Hotels would invest on renovation, executives went back to the drawing board to reassess what an appropriate Taj hotel should look like in New York. They concluded that it should be among the “finest” hotels, and so “wilfully and voluntarily”, Indian Hotels increased spends. In return, the lease was extended to 40 years. According to the original plan, the entire hotel was never meant to be shut down for renovation. But in December 2007, The Pierre was shut. By the time it reopened in 2009, the world was a different place. Goel says till it shut down, he never “sent a penny from India to support it”. But now, the entire proposition was in jeopardy.

Indian Hotels executives may dispute their execution abilities but they admit that the economy totally surprised them. After all, their plans hinged on economies behaving asynchronously. Goel says while the U.S. collapse created “new pressure points, the larger issue was the collapse of the domestic market”.

Between 2007 and 2009, revPARs fell from Rs 8,000 to Rs 6,000 and Indian Hotels hasn’t recovered. One way to interpret this is to see it as inappropriate capital allocation in assets at near-bubble levels. Could this have been done differently, through, say, management contracts, which would have used lesser funds (Four Seasons owns just two of the 90 hotels it runs)? Bickson thinks for a moment, and says “No”. He argues that while in West Asia and the Indian Ocean rim (Maldives, etc.) the Taj brand is known well enough to be handed management contracts, it still needs equity investment to demonstrate commitment in the West. “You need to put your money where your mouth is,” he says. And the payoffs are now happening elsewhere—such as the four Indian Hotels properties in China that are being taken on a management contract. On balance, Bickson believes that The Pierre is still a good deal, because they ultimately paid (all renovation included) “$627,000 a key to be on 5th Avenue for 40 years”, compared to other similar properties in New York such as the Mandarin Oriental and the Regent which were sold for $1.7 million and $1.4 million a key.

However, it is still adversely affecting share price and analysts continue to be anxious about it. Goel says that in the last few months, the weighted average tariff per room has moved to $650 per night (up from $300 when they took it over.) The goal is to take it to $850 a night, comparable to other top hotels in New York. “Even if we get to 40% to 50% of that gap, the hotel becomes profitable,” says Goel. With customers from Wall Street, The Pierre’s traditional clientele, having reduced, they are targeting folks from the entertainment industry as well as customers from Brazil, China, and West Asia.

Overall, the U.S. market has played spoilsport. Indian Hotels has been looking for the right hotels in Paris, Zurich, and London, where they’ve evaluated Somerset House and the Lanesborough Hotel. Bickson says he has always wanted a bigger presence in Europe (two properties in London currently). “Unfortunately, it [the U.S.] puts a dampener on the opportunities in London or Paris if something comes up. We are stuck because we went into one market.” Indeed, the revPARs of all the key international properties (see table) are slightly higher than Indian levels, even though those are in far more expensive economies. Indian Hotels is now planning to reinvent its Australia property Sydney Blue as a Vivanta.

There were other excesses (or capital allocation blunders) as well. In 2007, Indian Hotels invested Rs 102 crore in B-Jets, a Singapore-based fractional jet ownership venture. It bombed and the company now has a negative net worth. Its operations, marketing, and maintenance have been outsourced to Deccan Charters.

BACK HOME, THE story was playing out differently. It wasn’t just the speed of growth (10% annualised in over 10 years) but the sheer aggression of the foreigners. Back-of-the-envelope calculations using numbers from Bickson’s presentation show that between FY04 and FY12, Indian Hotels’ room share dropped from approximately 26% to 19%, on a growing base. He says the new operators are slashing management fees to win contracts and buying market share (what else would you do if you were new, and had deep pockets), whereas some things are a complete no-no for Indian Hotels. “I won’t cut my management fee from 8% to 4%,” he says. Then, to drive home the point, he says he evaluated the locations where the Four Seasons and the Shangri-La have come up in Mumbai (Lower Parel) but turned them both down. Four Seasons’ revPAR, according to estimates, is around Rs 9,000.

The key strategy that Indian Hotels deployed for growth here was to segment the market brand-wise and, depending on location and the tariff it could support, introduce the appropriate brand. Thus Taj was for luxury, Vivanta by Taj ‘upper upscale’, The Gateway Hotel was ‘upscale’, and Ginger was ‘economy’. This segmentation would allow pricing flexibility without any diminishing of the Taj brand. Ideally, Indian Hotels would own or have an equity stake in most of the Tajs, some of the Vivantas, and a few of the Gateways and Gingers. It was a sound plan, except that the slowdown took its toll. Indian Hotels signed 16 management contracts for Gateway Hotels between 2004 and 2008 with developers, but the poor economic conditions have delayed those projects.

Taj watchers say the Ginger move hasn’t been successful. When it began, the tariff for a single room was Rs 999. But given that they were typically located far away from city centres, the cost of transportation for users rose, who then began shunning them. And while Bickson and Goel say the team that set up Ginger wasn’t picked from Indian Hotels, former employees believe the mindset continued to be that of a full-service hotel. To scout for sites in and around Saharanpur (in Uttar Pradesh), employees “took private jets and a few choppers and spent almost as much money on reconnaissance [a few crores] as the land was worth”, says one former employee who declined to be named, but witnessed it first-hand.

At any rate, by late 2011, Ginger raised prices to between Rs 2,400 and Rs 4,700, pushing it into a segment where mid-level players such as Lemon Tree were present and offering superior facilities. This category, between ‘upscale’ and ‘economy’, is where a lot of activity is and represents a lost opportunity for Indian Hotels. Lemon Tree, the most talked-about brand in the segment, was built by Patu Keswani, former chief operating officer, Indian Hotels. Keswani, who studied trends in segmentation, figured that the key to success wasn’t so much branding, but more about getting the product and service right at the correct price. “In the U.S., which is a mature market, the brand owner has the power vs. the owner of the asset. In India, it’s the exact opposite,” he says. “Perhaps The Taj should have pushed for an expansion of its mid-market brand much earlier.”

Anshuman Magazine, chairman and managing director of commercial real estate services firm CB Richard Ellis, which does hotel valuations, says historically India never had quality three-star hotels. “Now that’s changing with business hotels such as Raintree and Lemon Tree, which give you five-star amenities like marble floors and premium bars, but at half the price.” Keswani’s advice for Indian Hotels: “Taj needs to get out of the areas where it doesn’t have a competitive advantage.”

SO WHAT IS its core competence? Over e-mail, the company says it’s “‘building sustainable relationships’ with guests, associates, partners, vendors, investors, lenders, and other stakeholders. We believe that with the effective combination of all these pillars, we have and will create value for the benefit of all concerned.” Old-timers say it is their legendary hospitality, making sure the guests are bowled over. But given its ambitions, Indian Hotels needs to see itself more as an infrastructure company with superior project management and capital allocation skills. (Goel admits that today hotels shouldn’t just be seen through a service sector lens.) In many ways, it’s the battle between bean counters and hoteliers. The trick is in figuring out the minimum threshold at which Indian Hotels will be able to command a premium. Does it need several people greeting guests at the reception area, or will one do? Given the earlier oligarchy environment, most Indian hoteliers are bad at this.

At Indian Hotels, the shift has begun, but it needs to gather momentum. Of the 120-odd hotels that Indian Hotels runs, 23 are management contracts, with no equity whatsoever. But of the 30 or so hotels coming up (outside Ginger), 23 will be run through management contracts, with zero equity from either Indian Hotels or any other Tata group companies. In other words, the model will completely flip going ahead. But it’s not just about lightening the balance sheet. It’s also about making sure projects come up on time.

There was a time when Indian Hotels was just about luxury. Then it wilfully reinvented itself. Now it’s playing a new game, where the rules are often set by others. That calls for relearning, and equally, unlearning

Leave a Comment

Your email address will not be published. Required field are marked*