SO MARK CUBAN WAS WRONG. The outspoken billionaire investor thundered in March that “we’re in a tech bubble—and it’s worse than 2000. The bubble today comes from private investors who are investing in apps and small tech companies ... and there is zero liquidity for any of those investments.”

After that you would expect the startup ecosystem to roll over and die, just like Lehmann Brothers did in 2008. Instead, I get a call at two in the morning from a bubbling 25-year-old who wants to discuss a “revolutionary” app. We spend the next 45 minutes chatting about prototypes, customers, markets, and seed money, before the former health-care analyst from Chennai decides to seek professional help from one of the “new accelerator guys”. I end the call wondering how these “guys”, my recent acquaintances Jim Duffy and Gabriel Fong among them, can cope with such enthusiasm 24/7.

Duffy and Wong are the latest in the accelerator space—think of them as the Jedi Masters who transform dreams on a drawing board to real businesses—to pitch their tent in India, having arrived here in early June. Duffy’s Entrepreneurial Spark (ESpark) works with over 350 startups in more than 40 countries, but India is its first full-fledged office outside Britain. Fong, a globetrotting investment banker-turned-entrepreneur from Hong Kong, has built an accelerator called Jaarvis. Within a couple of months of their entry, iPhone-maker Foxconn and payment giant Visa also marched in to set up startup foundries in India.

There were more before them. In February 2014, Toronto-based Ryerson University and its tech investment arm Ryerson Futures started a joint venture with the BSE Institute, a subsidiary of the Bombay Stock Exchange. The outcome was Zone Startups India, an accelerator housed in the BSE building in Mumbai. Last December, Ryerson Futures also tied up with India’s Chokhani Group to launch a $15 million (Rs 94.7 crore) fund that will annually invest $50,000 to $500,000 in early-stage technology businesses. However, it was the February entry of $73 billion Target, a Fortune 500 retailer based in Minneapolis (ranked 36 this year), which took the buzz to a different level. The company has run a tech support and operations centre in Bengaluru since 2005, but decided to tap into the country’s innovation talent to meet the challenges of a sector that’s increasingly technology-driven. The New York Times says Coca-Cola is planning something similar, while days before we went to press, Citi announced an accelerator to work with disruptive fin-tech startups.

So over half a dozen cross-border moneybags—I call them accelerators 2.0—in the span of 18 months, to say nothing of the early entrants, including Rajesh Sawhney-led GSF, Dave McClure’s 500 Startups, Microsoft Ventures, and more. What’s in this business to attract so many so rapidly, given the swirling talk about overheating? And what’s their game plan to win over local startups?

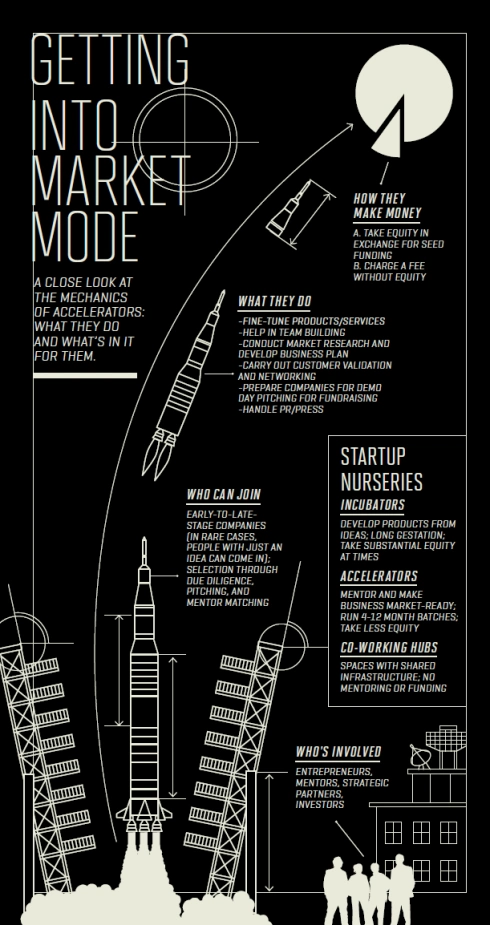

FOR THE UNINITIATED, accelerators are for-profit ventures that provide seed funding, spruce up the business model, speed up product/service development, offer mentoring, and connect fledgling startups with investors and customers. Most run four-to six-month programmes in exchange for equity, typically between 5% and 12%.

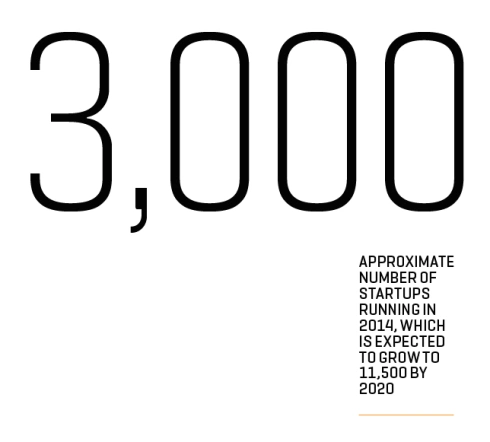

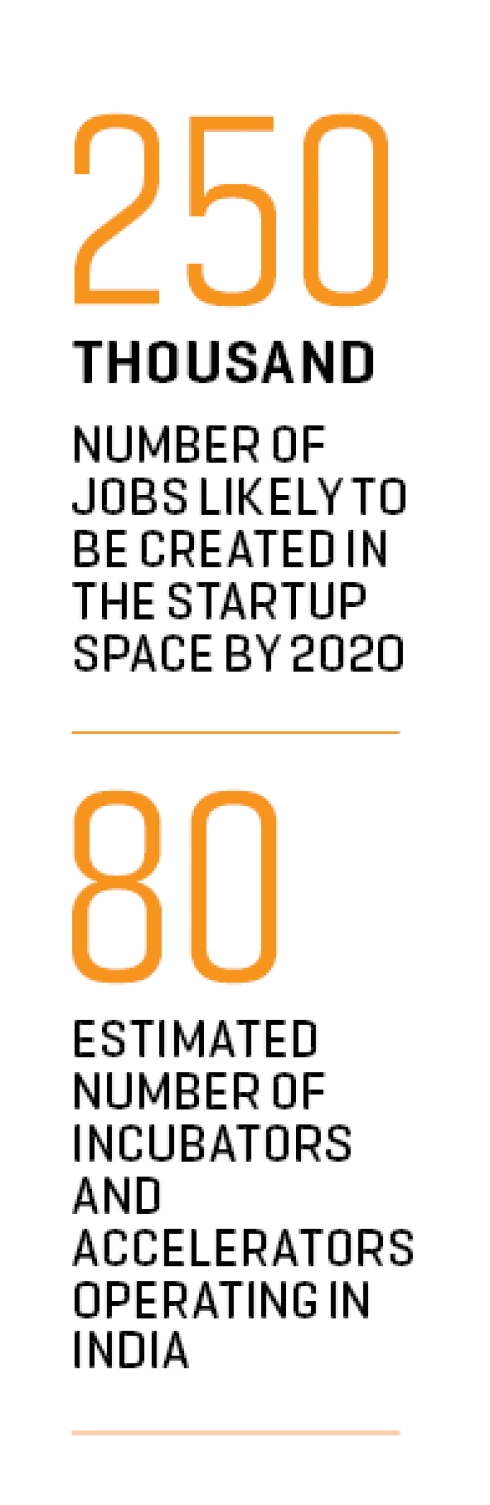

The biggest reason for the latest gold rush in this business is probably the malady called FoMo (Fear of Missing out)—you are in the “grab” mode and dare not let any opportunity slip by, at a time when startups are a sexy asset class with the promise of a blockbuster in every basement. The National Association of Software and Services Companies (Nasscom) says India is now the fourth largest startup hub in the world, with more than 3,000 of them. The number is expected to grow to 11,500 over the next five years, generating job opportunities for more than 250,000 people. Nasscom, too, has come up with a programme called 10,000 Startups that aims to set up as many companies over the next 10 years.

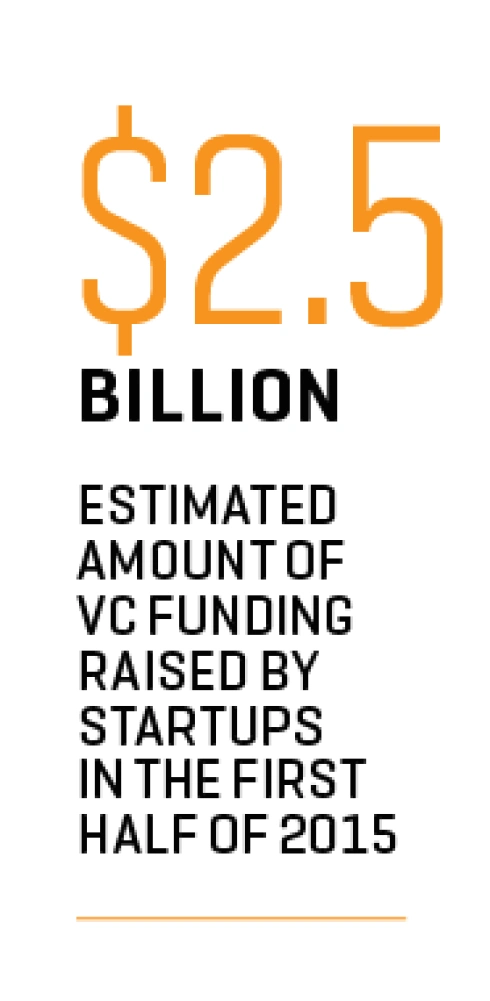

A funding tsunami has followed: Venture capital investors ploughed in between $2.4 billion and $2.9 billion in home-grown companies in 2014, compared with $1.8 billion in 2013, according to Dow Jones VentureSource. Last year, India was only behind the U.S. ($38 billion to $45 billion) and China ($4.5 billion to $5.2 billion) in VC funding. In the first half of 2015, it reportedly pulled in another $2.5 billion.

The frenzy notwithstanding, industry estimates put the number of accelerators and incubators (see graphic on next page to understand the difference) in India at a little over 80. “Too few, considering the growth rate”, says Ajay Ramasubramaniam, director at Zone Startups India. Then there are capacity constraints. Y Combinator, a star accelerator in Silicon Valley, hosts two batches a year. Its winter 2015 batch, the largest yet, had 114 companies. In contrast, an accelerator in India usually hosts five to 15 companies per batch.

The demand-supply mismatch is causing an unhealthy meritocracy, complain budding entrepreneurs. Even top accelerators are getting risk-averse and cherry-picking late-stage companies with proven traction. Both Microsoft Ventures and home-grown TLabs earlier told the media that the bar is getting higher for entrepreneurs all over the globe. But there’s another side to the story. “A lot of startups simply focus on the funding part, without putting any value to the other key services”—mentoring, team building, customer acquisition—“that accelerators bring to the table. But those are the services that help businesses grow,” says Ramasubramaniam.

Accelerator-hopping for better funding is a reality now. Meanwhile, good exits could be tough. In March, academics Yael Hochberg and Susan Cohen and Ph.D. student Dan Fehder published a list of the top 20 U.S. seed accelerators in 2014. (Y Combinator was not included due to certain criteria.) Overall, the startups that have graduated from the top 10 accelerators have a current total valuation slightly under $4.4 billion—but only 3.5% have exited successfully. It could take a decade or more for big exits to happen.

FOR DUFFY OF ESpark, the journey makes sense only if you are passionate about nurturing ideas that address underserved markets, especially in a country like India. “Given that many people will be starting out with a good idea, little funding, and no experience of business whatsoever, it’s the right time for us to come here,” he says. To find promising entrepreneurs (Duffy calls them “Sparklets”), especially in tier II and tier III cities, ESpark has formed a joint venture with Viridian Group, and is rolling out a series of “hatcheries” which will invest about $300 million in 300 early-to-growth-stage businesses in the first three years. The JV, which aims to create 10,000 jobs, has already shortlisted 23 businesses from diverse sectors, including unusual ones like poultry, apart from education, health care, e-commerce, and green tech.

“Every time the goal may not be creating a giant like Airbnb or Uber, nor an IPO,” says Duffy, when I ask him whether India has room for a model different from the aggressive growth focus of Silicon Valley. “A lot depends on the nature of the business and its ultimate ambition. It doesn’t matter whether they want to become global brands or remain within a niche.”

Isn’t that too benign an outlook in an age where everyone is hunting the next unicorn? “If you look at the number of jobs created by the businesses that reach the growth phase, you will see that investment in entrepreneurship is worthwhile even with a 60% failure rate,” says Duffy.

There’s a different vibe at Jaarvis’s 20,000 sq. ft. co-working space in Gurgaon. The facility can accommodate up to 50 startups, most of them hard-core tech companies from areas like the Internet of Things. Jaarvis is setting up a fund to support its portfolio companies and expects to sign up to 15 startups for its first class. It’s planning three batches a year and will take 7% to 15% equity.

Unlike ESpark, Valley-esque fast growth is Jaarvis’s watchword. “Hit the market in 90 days, else you’re dead,” emphasises Amit Dang, vice president, technology delivery. “Right now, another team could be doing the same thing someplace else and doing it faster.”

Founder Fong’s resume helps understand the accent on speed. After more than two decades in the private equity and venture capital space with the likes of Och-Ziff Capital, Morgan Stanley, and Goldman Sachs, Fong launched his debut venture GoGoVan, a last-mile logistics solution, in 2013. Within a year, the business scaled up from Hong Kong to about 10 cities, in China, Korea, Taiwan, and Singapore. Later that year, he co-founded Jaarvis Technologies, along with Indian colleagues Jaspal Sarai and Kuldeep Bhayana (he is no longer with the company)—in addition to five other ventures. “Because we are running our own startups, we understand the technology, the market, the challenges. That makes the critical difference,” he says.

Fong contends that the real value of an accelerator lies in mentoring—not part-time lip service but active, intense, and insightful guidance. That’s a key mandate to Jaarvis’s India team of 100-plus professionals, who will handhold the newbies across every area of business—from technology to marketing to networking and fundraising. “Frankly, that’s the most invaluable resource,” says Fong. “Funding will be wasted if startups constantly make mistakes.”

Ankit Khanduri, whose maiden venture Spotwrks (a talent-acquisition platform) is in the first batch, tells me why he chose Jaarvis. “Most accelerators I talked to were looking for mature products. But mine was at a concept stage and needed a lot of work. Jaarvis liked the idea and helped us with the development.” A GSF or TLabs might have helped him raise a bigger round on Demo Day, but Khanduri was drawn by the prospect of a partnership with Jaarvis and accessing global markets at an early stage of its lifecycle. “That’s the kind of growth we need, not just the money,” he says.

Zone, which has worked with over 50 startups till date, stresses resource pooling. “Accelerators can’t afford to slot their stakeholders in just two large categories [startups and investors] if they want to build a thriving hub,” says Ramasubramaniam. So his organisation works with academic institutions for internships and live projects with the startups that have enrolled at Zone. It will soon start a programme to help build a talent pool that startups can hire from. Over the past four months, it has brought in close to 70 interns to work with its startups. It has also tied up with corporates to conduct hackathons and create rapid prototypes—it’s a small source of revenue that helps subsidise expenses.

Zone itself operates like a lean startup and doesn’t offer funding early on. “We work like co-founders without equity, and help our companies crack key customers,” says Ramasubramaniam. “Our international connection comes into play only when there is a desire and readiness to enter the Canadian market.”

Meanwhile Target, which started its third class in July, has a markedly different approach. “We do have a [narrow] focus on retail, but our value proposition is strong,” says Target India president and managing director Navneet Kapoor. “[Unlike other accelerators,] here you find a deep business context and solve problems for tens of millions of customers.”

For each batch, Target picks five startups from about a thousand applicants. “The goal is to get their products to a proof-of-concept or test-and-learn phase,” Kapoor says.

The benefits are many. For one, the products developed get pilot-tested on a global scale. “When the class is over, we may retain the startups as vendors or we may buy their technology. Or if we really like the technology and the people, we may buy out the company. Or if we just like the people, we may choose to acquihire. The possibilities are endless,” says Kapoor. The big vision? “The India accelerator will be an integral part of our future innovation strategy, like our San Francisco centre,” he affirms.

DESPITE ALL THE ACTION, it’s unclear whether accelerators are good business. Venture building is no longer the exclusive preserve of accelerators as all and sundry seem to be falling for startups—governments, corporate houses, even the hoi polloi wooed on crowdfunding platforms. But there’s one critical difference: Accelerators need to follow the old tenet of return on investment, or face the fate of The Morpheus, India’s oldest such business with 80-plus companies in its kitty, which was forced to shut last year after chronic losses.

Many feel that the bottom-up approach of Duffy would work best: There’s a vast social enterprise market yet to be cracked, and only a few accelerators like Chennai-based Villgro and Sandbox Startups, which has offices in India, the U.S., and Canada, are exploring it.

Then there’s the unique model followed by Mumbai-based Sparknext, which plays a key role across the entire value chain—from sourcing hot ideas to development to funding. Founder Ahmed Aftab Naqvi says Sparknext identifies high-growth markets and invests in ideas that come from a network of industry experts, angels, and VCs—as opposed to just first-time entrepreneurs. It then finds the people who can run with those ideas.

Focussing on specific niches, à la Target or even Jaarvis, is another preferred trail. In his post on the news site VentureBeat, Bryan Bulte, co-founder of Texas-based accelerator Seed Sumo, says more vertical accelerators will come into play this year. Right now, 95% of accelerators focus only on early-stage companies, he writes. Expect to see programmes opening up to later-stage companies, which can fetch bigger returns. If that happens, accelerators could be taking the fight to the large VCs. In India, the Securities and Exchange Board of India or SEBI, the country’s stock market regulator, recently relaxed listing norms for startups. This may encourage seed-stage funders like accelerators to stay invested and take part in typical VC rounds, now that there will be more liquidity and better exit opportunities. To counter such possibilities, global VCs have already started backward integration to create “startup studios”, which offer a convenient combo of an accelerator, a co-working space, and access to VC funding.

But ultimately, says Naqvi, no accelerator can thrive “unless there is accountability”. Founders often lose valuable equity without any tangible gain because most accelerators don’t care much about the outcome. In contrast, “we don’t take equity until a startup raises its first round of funding”, says Naqvi. “We also offer an option to exit Sparknext halfway through the programme without giving us any equity, if a team feels it is not benefiting from the experience.” Last year, top U.S. accelerator Techstars also announced an equity-back guarantee if a company is not satisfied, but most players in India are far from that kind of derring-do.

Not everyone sees the need for a radical change. Poornima Vijayashanker, venture partner at 500 Startups, bets on the current model, saying accelerators increase a startup’s credibility because they’ve made an investment at a very early stage—thereby de-risking it for other investors. The legal support and guidance they provide in the early days gives future investors peace of mind.

Ramasubramaniam thinks there’s room for various models to coexist here, along the lines of Silicon Valley or Israel. “As for our companies, many of them may not be glamorous like Airbnb or Uber,” he says. “But several of them are serious startups, developing technology solutions which sit at the back end of such [star startups]. That speaks of their value.”

Dang of Jaarvis agrees. “Entrepreneurial heroes are those who can tweak products, services, and technologies to build on local markets,” he says. “Take the hyperlocal startups that have solved India’s notorious logistics problems. We get to see these innovations every day from scores of companies.” Dang believes the boom is here to stay and “more people will need accelerators to get business-ready”. Never mind the shrill doomsday prophecies from Mark Cuban’s ilk.

Leave a Comment

Your email address will not be published. Required field are marked*