When bengaluru-based serial entrepreneur Meena Ganesh wanted fresh funding for her home health-care company Portea Medical last year, she was not keen to give up more equity. Ganesh and her husband Krishnan had already diluted some stake to raise a $9 million (Rs 48 crore at the time) venture capital round. This time, they decided to settle for a $4 million cheque from Mumbai-based venture debt firm InnoVen Capital, which would sustain Portea’s growth until it was ready to raise the next VC round. “We knew the InnoVen team, and the money helped extend our runway,” says Ganesh. It was essentially a short-term loan, so why didn’t she go to a bank instead? “Banks don’t have suitable debt instruments,” Ganesh dismisses the idea. “They are not at all tuned to working with startups.”

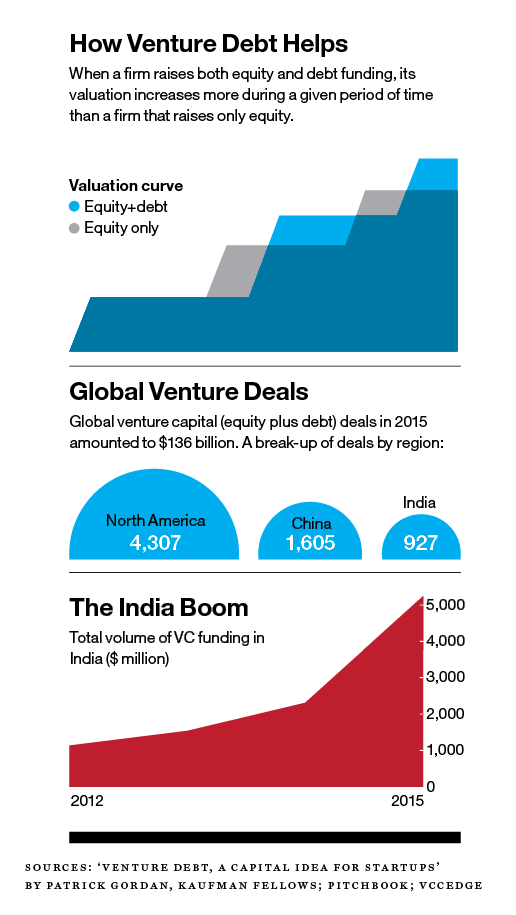

Ganesh’s sentiment resonates beyond startups. According to World Bank data, about 70% of all micro, small, and medium enterprises in emerging markets suffer from the lack of institutional finance. Venture debt firms such as InnoVen, Trifecta Capital, Oliphans Capital, and IntelleGrow are trying to build robust businesses by addressing this gap. The model is simple—they raise money from institutional investors and lend to startups, the average ticket size varying between Rs 2 crore and Rs 30 crore. But unlike traditional venture capital investments that involve intricate due diligence and long-term equity grab, venture debt mostly comes as unsecured, short-term loans to early-stage companies that need working capital.

“Any debt needs collateral, profitability, a track record, maybe an industry that banks are comfortable lending to. But we have turned [the concept] on its head,” says Vinod Murali, managing director of InnoVen, one of the earliest players in this space, which was founded in 2008 as a non-banking, non-deposit-taking financial company. “We’re far cheaper than equity deals, but our biggest value lies in the fact that banks in this country don’t lend to startups. A cement company with a turnover of Rs 200 crore is different from an e-commerce company with a turnover of Rs 500 crore. Banks understand cement, [but they don’t get e-commerce].”

InnoVen lends to startups at 15% interest, which doesn’t vary too much from borrower to borrower. “There isn’t [too much difference in the] credit risks associated with cash-burning startups,” says Murali. The company, which claims to be the largest debt financer of early- and mid-stage startups, has a portfolio of about 70 investees, notably Snapdeal, Myntra, FreeCharge, FirstCry, and MobiKwik. “Of the top five startup exits in India, we’ve been part of three. We were in Prizm Payment that Hitachi acquired, in Myntra acquired by Flipkart, and in FreeCharge acquired by Snapdeal,” says Murali.

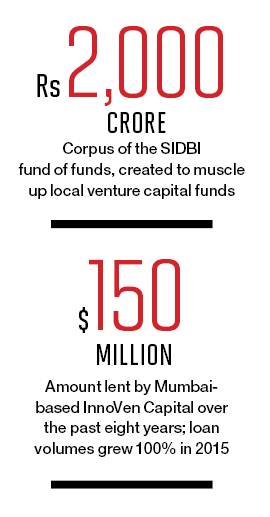

InnoVen recorded 100% growth in loan volumes in 2015 and has lent $150 million over the past eight years. It is now planning to expand to China, Indonesia, and Malaysia.

TO BE SURE, InnoVen’s growth is an exception; debt funding is still a fuzzy idea in the startup ecosystem. Indian startups, especially tech startups, have had little need to look beyond venture capital; they were at the centre of a much-documented investment boom last year. But growing concerns about profitability have put the brakes on the funding glut. The days of frothy valuations also seem to be over. Recently, Morgan Stanley Institutional Fund Trust, a minority investor in India’s largest e-commerce company Flipkart, devalued its holdings in the firm by 27%, bringing the enterprise value to around $11 billion against Flipkart’s own estimate of $15 billion. The bottom line: These are hard times for startups looking to raise quick funds or big money. Debt could offer a way out.

However, debt comes with its own caveats. Lenders need to be repaid within a specific time period (usually 24-48 months), no matter how the business fares. Apart from the interest, which can be steep for a fledgling company, many lenders ask for an equity kicker—a clause that allows them to take equity share in the borrowing company some time in future. If the stock goes up and the company eventually gets acquired or listed, the lender can activate the equity kicker and mop up a profit.

Also, notwithstanding Murali’s claim that debt funders are more easy-going than their VC counterparts, many—including InnoVen—only lend to companies that already have strong VC backing. Or if the borrower is about to raise a big round, as was the case with Portea. “Venture debt cannot substitute equity funding. It provides an extra layer on the back of VC funding,” says Murali. (InnoVen often picks up deals from its network of VC contacts and helps portfolio companies meet potential investors for their next round of funding.) Delhi-based Trifecta Capital, a new entrant in the space, also ignores companies unless they have raised at least one round of VC funding.

Smaller funds like Mumbai-based Oliphans Capital see an opportunity in lending to bootstrapped companies that others won’t touch. Anish Jhaveri, founder and chief executive, says he doesn’t care if the companies coming to him have not raised any funding. “We lend for a maximum of 90 days. It takes us just a couple of days and a few calls to run a background check on the borrower.”

Another Mumbai-based firm IntelleGrow—the venture debt arm of Aavishkaar Venture Management, which was set up to “catalyse development in India’s underserved regions”—also doesn’t fuss over VC backing. “For 38% of our companies, we’re the first lender,” says COO and CFO Nitin Agrawal. “We don’t take equity in all our companies, so we mostly rely on operating cash flows,” he adds. IntelleGrow hedges against the risk of betting on very early-stage companies by charging a relatively higher interest rate of 18% to 20%.

A KEY CHALLENGE for the debt sector is to get banks to loosen their purse strings. Unlike U.S. startups that can obtain cheap, flexible loans from the likes of Silicon Valley Bank (SVB) and City National Bank, Indian banks haven’t warmed up to the idea. Both State Bank of India and HDFC have started entrepreneur-specific services, but refrain from actual funding.

Trifecta, which has raised Rs 500 crore for its Venture Debt Fund I, made a start by signing up Ratnakar Bank (RBL), a Fortune India 500 company, as its biggest investor, with a contribution of Rs 50 crore. “Back in 2008 when I was with Clearstone Venture Partners, I knew that Vishwavir [Ahuja, MD and CEO of RBL] was very keen on fintech and payment solutions,” says Rahul Khanna, Trifecta’s co-founder and managing partner. “Now RBL provides tailored services to some of our portfolio companies, just like SVB does in the U.S.”

At least one public sector entity, the Small Industries Development Bank of India (SIDBI), is also trying to make the banking sector more participative, albeit indirectly. Last August, finance minister Arun Jaitley launched the Rs 2,000 crore India Aspiration Fund, a fund of funds administered by SIDBI, with the goal of muscling up local VC funds. “Our aim is to keep local funds well capitalised, so that Indian startups can stop relying on external funding sources that have inherent vulnerabilities,” says SIDBI chairman and managing director Kshatrapati Shivaji. “However, venture debt funding is not a conventional space. Our institutions are not equipped for it and the financial regime in our country is also slightly conservative; so it will take time to mature.”

The regulatory outlook around funding to unlisted companies has been patchy. In 2012 the Securities and Exchange Board of India created privately pooled investment vehicles called alternative investment funds, which include debt funds servicing unlisted companies. “We found it much easier to set up a fund and return the money to our investors [periodically], instead of setting up an NBFC (like InnoVen) and acquiring equity [which entails a longer wait],” says Khanna of Trifecta.

The country’s foreign capital regulations also tend to make the venture debt market shallow. “The majority of VC firms in India operate foreign funds. But external commercial borrowing norms in India cap the interest rate [that a foreign lender can charge], benchmarked to Libor. Therefore, very little FDI money trickles into startups,” says Thomas Hyland, co-founder and partner at Hyderabad-based venture equity firm Aspada Ventures. Under Reserve Bank of India norms, Indian firms can borrow up to 300 basis points over six-month Libor for three-to-five-year-long loans. But Hyland says that’s not nearly high enough to compensate foreign lenders for the high risk they take. “You don’t see the same kind of restrictions on rupee funds.”

IN ORDER TO BOOST the credibility of the sector and encourage more lenders, Pune-based startup GREX has launched an invitation-only online platform that allows investors to discover, track, and invest in unlisted companies. Founder and CEO Manish Kumar also plans to open up debt funding on the platform, which will have the added benefit of bringing visibility to unknown SMEs.

“Today, if an SME gets a loan, nobody is the wiser because there’s no platform to discuss it,” says Kumar. If unlisted companies and their investors can publicly record these deals, the market will be aware of their credit records, and banks can use that data for their due diligence. GREX has signed up with credit-rating agency CARE Ratings, which will grade the companies on its platform. In addition, the firm is setting up a secondary market for investors to buy and sell shares of member companies on the platform.

Abhijit Agashe, executive director, GREX, says there’s no reason why banks should not be interested in lending to these companies. “If you lend to a Tata or Reliance, the margin can be as low as 0.3%. But lend to an SME and you can earn up to 3%.”

If his high-risk, high-return logic persuades bank bosses harrowed by non-performing assets, it could signal a win-win for the ecosystem.

Leave a Comment

Your email address will not be published. Required field are marked*