Even as the coronavirus contagion rages around the world, there was another contagion threatening to build up in India’s financial sector over the past few months. YES Bank, the country’s fifth-largest private sector banking entity (with assets of ₹2,90,985 crore) co-founded by flamboyant banker Rana Kapoor, was teetering on the edge of collapse.

Several attempts by the then managing director and chief executive officer Ravneet Gill to bring in funds from new investors failed as mounting nonperforming assets (NPAs) threatened to derail the bank. This contagion, if left unchecked, would have led to another IL&FS-like disaster, only with even greater impact

But finance minister Nirmala Sitharaman and Reserve Bank of India (RBI) governor Shaktikanta Das stepped in. On March 5, the finance ministry announced a moratorium on the bank, capping withdrawals at ₹50,000 a month (on the eve of the day when withdrawals were banned, deposits had fallen to ₹1,37,506 crore—a 17% drop in just over two months). The board was dissolved and an administrator, former State Bank of India (SBI) deputy managing director and chief financial officer Prashant Kumar, was appointed (he has since been renamed as the MD & CEO of YES Bank).

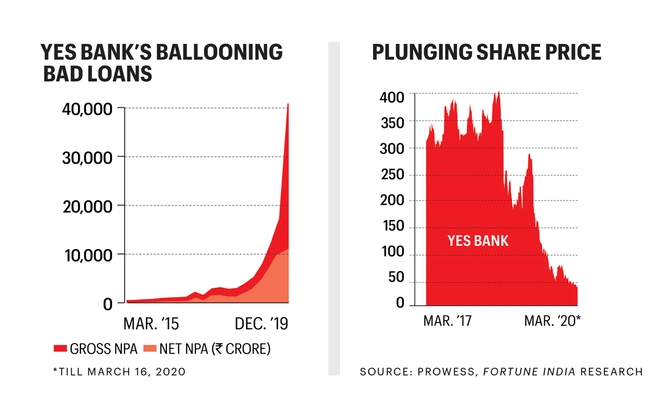

The next day, the RBI announced a draft reconstruction plan for the bank where SBI, the country’s largest lender, would pick up a maximum of 49% in the reconstructed share capital of the bank. After the announcement, YES Bank’s stock price, which had been in free fall in the wake of the moratorium, touching its lifetime low (intraday) of ₹5.55 on March 6, stabilised.

The government and the RBI clearly seem to have weighed the odds before deciding that a community bailout with many banks chipping in was the best way to ensure there was no further danger to the financial system.

SBI has pumped in ₹6,050 crore, and will hold two board seats. Several other entities have said they would pick up equity totalling ₹3,950 crore: Housing Development Finance Corporation (₹1,000 crore), ICICI Bank (₹1,000 crore), Axis Bank (₹600 crore), Kotak Mahindra Bank (₹500 crore), Federal Bank (₹300 crore), Bandhan Bank (₹300 crore), and IDFC First Bank (₹250 crore).

The government and the RBI are taking no chances with the reconstruction scheme: It has mandated a lock-in on 75% of the shareholding of every shareholder who has more than 100 shares as on March 13 (the day the scheme was notified) for three years. SBI cannot reduce its shareholding below 26% in this period. And those who invest will be exempted from paying capital gains tax. This, however, is only the beginning of a long and arduous journey for the new management. The constant flow of negative news about the bank had shown that there was something seriously amiss with the bank, but how serious no one could tell for sure.

That confusion cleared up when YES Bank announced its third-quarter results for FY20. It posted a quarterly loss of ₹18,564.25 crore. NPAs rose 58% to ₹40,709 crore in this period, up from ₹17,134.4 crore a quarter ago.

Now stakeholders are trying to spread the feeling that “All’s well that ends well.” The RBI chief said the bailout was a good example of a public-private partnership and YES Bank’s revival was “credible and sustainable”. The underlying theme of the effort, he said, was to protect depositors’ interests.

But not everyone shares the RBI governor’s optimism. Nomura analysts Amit Nanavati and Tanuj Kyal, while suspending coverage of the bank’s stock, say that while the bank’s “going concern risk” is now minimised, the lender is “damaged beyond repair”. “The reconstituted board... will need more turnaround experts/ bankers, while regulatory oversight too will have to be upgraded and tightened at the regulator’s end,” say Anand Dama and Neelam Bhatia of Emkay Securities after the bank announced its results. This view seems to be in line with what the bank’s statutory auditors, BSR & Co., have said.

The outlook, the auditors said, depends upon the degree of success of the final reconstruction scheme, the quantum of capital infused into the bank, and its ability to stabilise deposit balances. Also, there have been debates as to why the central bank, which in 2018 had refused to extend Kapoor’s tenure, did not act sooner despite widespread fears about the health of the bank for the past few months now.

The other issue is the question of moral hazard in a government-sponsored bailout of a private lender. “Any bailout of a private sector entity by PSUs [public sector undertakings]/government/taxpayers indeed creates a moral hazard,” says Suresh Ganapathy, an analyst at Macquarie. “Unfortunately, the cost of not bailing out YES Bank for the economy and the banking system is far higher than bailing out,” he points out.

With the economy in the doldrums, and amid the Covid-19 scare, India can well do without another IL&FS. “Under the current circumstances this [a bailout] looks to be the only option,” says Ganapathy.

Leave a Comment

Your email address will not be published. Required field are marked*