Bank of Maharashtra (BoM) has come a long way from exiting the prompt corrective action (PCA) framework in 2019 to industry-beating growth and emerging as the best bank in the PSB category in Fortune India-Grant Thornton Bharat Best Banks study. A bank is put under PCA when it performs poorly on asset quality and profitability.

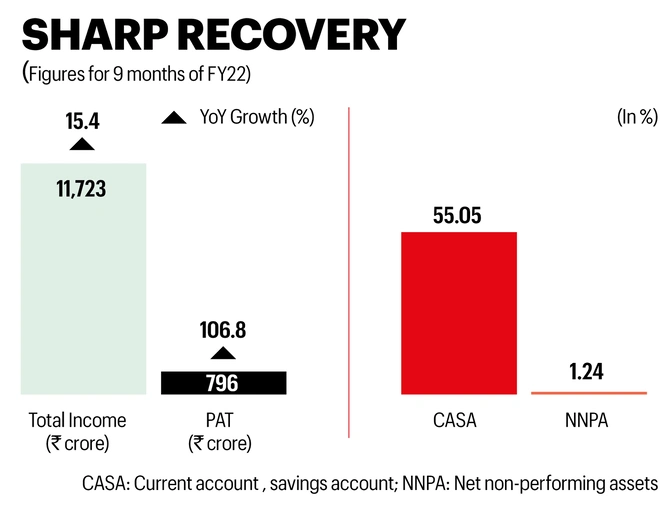

The dramatic change in fortunes has been driven by MD & CEO A.S. Rajeev, who took over in December 2018 when BoM was in a critical situation. Former CEO Ravindra P. Marathe had been arrested in a loan fraud case. Asset quality, profitability and non-performing assets (NPAs) were at crisis levels. The new MD & CEO effected systemic changes even as government injected capital. Three years on, total business grew 18.27% year-on-year to ₹3,15,620 crore in December quarter of FY2022. Deposits rose 15.21% to ₹1,86,614 crore as on December 31, 2021. Gross advances rose 22.98% to ₹1,29,006 crore. “Financials became better as anticipated along with significant internal improvement in systems. Focus on balance sheet, quality of credit, employee morale and structural changes to reduce operational costs helped us,” says A.S. Rajeev.

Credit Check

BoM introduced a three-pronged system to assess credit quality. First was credit check at branch level. This was followed by due diligence by an external agency and finally an end-to-end check by the sanctioning authority. “We follow a bottom-up approach in credit assessment,” says Rajeev. “Earlier, percentage of corporate loans was too high. The board decided to focus more on RAM (retail, agriculture and MSME) portfolio. Now we maintain 60:40 ratio between RAM and corporate loans. We have been able to register 25% growth in RAM, which remains the driving force of our loan book,” he adds.

Asset quality trends are encouraging as well. Net NPAs were 1.24% in Q3 of FY2022 compared to 2.59% a year ago. Gross NPA ratio declined from 7.69% to 4.73%. The bank is expected to improve NNPA and GNPA to ratios to 1% and 4%, respectively, in year ended March 2022 as a direct result of new loan recovery systems. Early warning signal and credit monitoring module have been integrated with loan lifecycle management system. “Once an account becomes special mention account (SMA-0), all efforts are made to recover dues before it turns into SMA-1. The bank has established an exclusive loan tracking system where our staff regularly follows up with borrowers,” says Rajeev.

BoM has also worked on cost reduction with the help of automation and technology adoption. For example, it has changed the ATM installation model from operating expenditure (where a managed service provider deploys and operates ATMs) to capital expenditure (bank installs own ATMs).

The bank has also put in place an e-surveillance mechanism for ATMs to reduce the cost of providing physical security. Besides, it used to outsource some IT functions. “The cost of outsourced employees is three times more than our own employees. So, we have recruited adequate number of IT experts in last two years. This has improved quality and reduced costs,” says Rajeev.

The Digital Bank

Covid-19 has led to overhauling of banking operations. “Post Covid-19, we learnt that many more processes could be automated,” says Rajeev. BoM established a digital banking division to give more thrust to digital journey and facilitate digital lending and other digitally-enabled services. It has partnered with NBFCs like Lendingkart, MAS Financials and Loantap under the co-lending model wherein it is rolling out cash flow-based lending. It has also set up a digital marketing vertical.

A well though-out roadmap is helping it take slow and smart steps.

Leave a Comment

Your email address will not be published. Required field are marked*