When the likes of Swiggy and Zomato were flirting with their quick commerce grocery delivery service last year, a new kid on the block, Zepto, took the market by storm. At the peak of the Covid-19 pandemic, Zepto promised to deliver over 2,500 products in 10 minutes. Its founders — Aadit Palicha and Kaivalya Vohra — are all of 19 years who dropped out of their under-graduate programmes in Stanford University to launch the grocery delivery platform. And in less than a year, Zepto secured a valuation of over $570 million.

India’s start-up ecosystem has plenty of stories of college drop-outs and entrepreneurial geniuses who have carved successful businesses out of their hostel rooms. It’s no surprise then that the bulk of the 2022 edition of Fortune India’s 40 Under 40 list comprises smart entrepreneurs running highly disruptive yet successful start-ups. A closer look at their journey, however, reveals that these founders are far from being casual entrepreneurs. Their businesses may be innovative and highly disruptive (an area where a legacy company wouldn’t have ventured into), but they have had their stint in traditional businesses before coming up with successful models.

Byju Ravindran and Divya Gokulnath were teachers before they launched Byju’s. Their professional stints helped them understand issues concerning students across the board. Similarly, Ajaita Shah worked with micro-finance companies for seven years before launching her rural supply chain start-up, Frontier Markets.

Legacy Organisations Matter

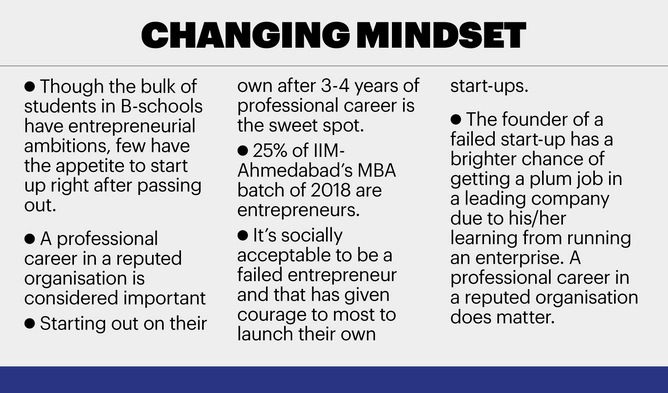

India may have created 45 unicorns in 2021, but nine out of 10 start-ups fail in India, according to analysts. Millennials are aware of the fact. While school dropouts such as Ritesh Agarwal (founder of Oyo Rooms) are role models, new-age professionals know that they are exceptions. “We just have two-three students every year who want to launch their own start-up immediately after passing out of business school. At IIM-Ahmedabad, there is a huge attraction for corporate placements. However, the sweet spot to turn into entrepreneurs is after 3-7 years of professional experience,” says Amit Karna, professor, strategy, IIM-Ahmedabad. Around 25% of students from the 2018 batch have their own start-ups today, but starting up wasn’t their first choice.

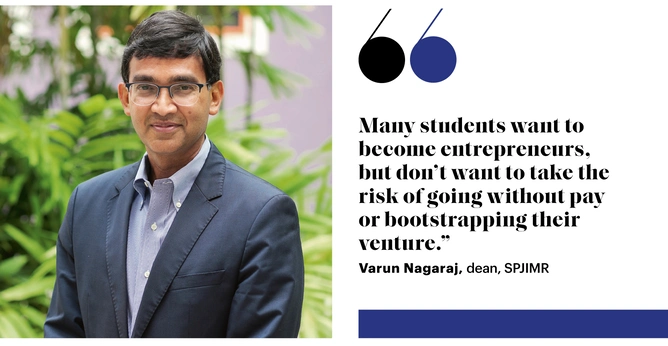

According to Varun Nagraj, dean, S. P. Jain Institute of Management and Research (SPJIMR), most of the successful start-ups are in the B2B space such as supply chain or food processing, but a majority of those who cracked it have had experiences of working in large organisations. “These are insights you will not get after coming out of undergraduate institutes or business schools. These are insights you will get after working in a cold chain. B2B is best pursued by somebody who has worked for certain number of years and identified that the existing solutions are inadequate and how it can be better,” explains Nagraj.

The Power of The Pay Cheque

Upamanyu Acharya, an MBA from the 2021 batch of IIM-A, agrees that it isn’t easy to start up immediately after business school. “The two years at a B-school have made me realise that India is a complex market. I need to have a deeper understanding in order to launch a start-up. And to get that, it is necessary for me to work in a legacy firm.”

Acharya currently works in the digital marketing arm of a leading FMCG company. He will wait before starting a new venture. The experience of running a cryptocurrency and blockchain content start-up during his under-graduation days has taught him that raising capital isn’t easy. “Today if I were to do a risk-reward analysis, I am not sure if running a start-up would give me the kind of remuneration my MNC job is giving me.”

Apart from the desire of working in a blue-chip company, most B-school graduates, especially those who go to Tier-I cities, also have the pressure to pay off education loans. The course fee of IIMs or the likes of SPJIMR or XLRI is in the range of ₹24-28 lakh and that’s one of the reasons why most business school graduates prefer a job to launching their own start-up. “Many students probably want to become entrepreneurs, but don’t want to take the risk of going without pay or bootstrapping their venture. They need access to lakhs of resources — and these are middle-class students,” says Nagraj of SPJIMR.

Professor Janat Shah, dean, IIM-Udaipur, says he has at least five-six students every year who have ambitions to start up soon after their MBA. “We allow these students to pursue their own ventures instead of doing summer training. We have an incubation centre, which funds their venture partly. We also give them a stipend of ₹10,000 per month to meet their expenses, but they have to work under faculty guidance.” If their start-up fails within a few months of completion of their MBA programme, IIM-Udaipur also allows them to return to the campus and participate in the placement process.

Shah says there is barely one student in every batch whose start-up actually takes off and the remaining come back to join the placement process. “We also have 5-6 students every year who would have had a failed start-up and then joined us to pursue MBA.”

“A lot of failed entrepreneurs are going for MBA as it gives them confidence to launch a new start-up,” says Kanwaljit Singh, founding partner, Fireside Ventures. In fact, a lot of students who are clear that entrepreneurship is their calling even choose to begin their career in a successful start-up rather than join a legacy company.

Youngsters look for inspiration, mentorship and learning from successful entrepreneurs and businesses, says Aditi Pareek, head, human resources, Pepperfry. “The flat organisational culture in start-ups enables and encourages employees, especially new joinees, to engage with the senior management. This provides them the opportunity to adapt faster and engage with multiple employees across levels and functions, thus giving them an understanding of not just the depth but also the width of the business.”

Daring to Win

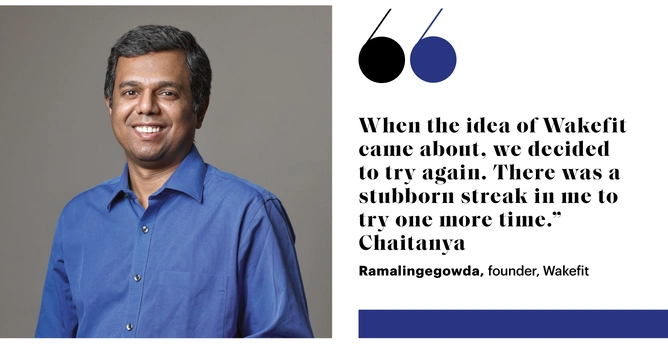

Home furnishing and furniture firm Wakefit’s founder Chaitanya Ramalingegowda’s first tryst with entrepreneurship was at the age of 16 when he started a spoken English class at his aunt’s garage in Mysore. Though the venture had students, he decided to fold it up and focus on studies. After engineering, he worked with two IT firms and then studied MBA at ISB Hyderabad. For a brief period, he worked with Deloitte in the U.S. and that’s when the entrepreneurial bug bit him again. “I was being paid to give advice to a global CEO who was listening to a 29 year old, because I had something to say based on logic, data and analysis. I began to wonder why I couldn’t use all that logic, data and analysis to start my own consumer-facing business,” explains Ramalingegowda.

He gave entrepreneurship a second shot in 2011 at the age of 30. Over the next few years, he launched two start-ups, but both failed. Left with just ₹800 in his bank account after the closure of his second venture, he had no option but to go back to a full-time job. It was then that he met Ankit Garg, the co-founder of Wakefit. “When the idea of Wakefit came about, we decided to try again. There was a stubborn streak in me to try one more time.” There has been no looking back since. Wakefit currently is a ₹416-crore profitable enterprise.

As IIM-A’s Karna points out, the sweet-spot for most B-school grads to embrace entrepreneurship is after acquiring professional experience of at least 3-7 years. By that time they are mostly in the age-bracket of 27-30, done with their educational loans, and are all set to jump into the entrepreneurship bandwagon.

Manish Taneja, Rahul Dash and Suyash Katyayani, co-founders of online beauty and personal care marketplace, Purplle.com, were 27 and 26 year olds when they launched their venture. By then Taneja had worked with Avendus and Fidelity, and Dash with Tata Administrative Services. “I got an opportunity to set up Tata Sampann’s supply chain in Pondicherry and also got a chance to participate in a lot of its other 0-1-year-old businesses. In fact, the TAS experience drove me to entrepreneurship,” says Dash.

Katyayani is, however, the classic engineer-turned-entrepreneur, who stepped into the world of entrepreneurship within months of his professional role at telecom firm OnMobile. “The year I joined was their IPO year. It was a company incubated out of Infosys and within eight years the founders had brought it from a start-up stage to IPO. I could see young people getting rich, which was inspiring. Also, I was in Bengaluru and every café you went to would have a venture capitalist conversation happening.” By the time Katyayani joined Purplle as CTO and co-founder, he was a serial entrepreneur who had launched and shut down three start-ups.

Once you are an entrepreneur, the mindset changes from being risk-averse to having an insatiable risk appetite. “Today, it is socially acceptable to fail, and that is making all the difference,” says Rohit Bhayana, founder, Lumis Partners. “If they fail they can go and work in a firm or join another start-up. An ecosystem of entrepreneurship is getting created and this will get accelerated,” he adds.

Retention Tool

Even legacy companies such as Unilever, ITC, L’Oréal and Marico are creating entrepreneurial opportunities for employees as a retention tool. Hindustan Unilever has a concept of CCBTs (country category business teams), which straddle across home care, laundry, hair care, skin care, naturals and food and function like mini-boards within the company. Each CCBT is headed by a general manager (the average age of a GM is between 27 and 30 years), who has his/her team of finance, marketing, innovation, supply chain and digital professionals. The CCBTs are not just empowered to run their businesses like entrepreneurial ventures, they also have a say in mergers and acquisitions.

Singh of Fireside Ventures says large corporations are more than happy to hire a failed entrepreneur. “The person with his/her learnings is considered an asset,” he adds.

The writing on the wall is clear — while legacy companies will continue to flourish, millennial Indians will increasingly embrace entrepreneurship. Just as you will find in the journeys of Fortune India’s 40 under 40 winners for 2022.

Leave a Comment

Your email address will not be published. Required field are marked*